Chicago Booth and NYU Stern remain the two non-Wharton programs that finance employers prioritize.

NYU Stern placed 28.0% of its Class of 2025 into Investment Banking against Chicago Booth's 8.3%, both at a $175,000 median base salary. Chicago Booth placed 5.3% of the class into Private Equity against NYU Stern's 1.3%, anchored by Steven Kaplan's Entrepreneurial Finance and Private Equity course. NYU Stern's Aswath Damodaran teaches the canonical M&A curriculum.

For the 2026 Comparison, I look at the latest employment reports that the two schools published for the Class of 2025, and evaluate finance sub-industry breakdowns to find whether Chicago Booth or NYU Stern MBA is a better fit for your Finance career.

TL;DR (At a Glance)

- Stern is the stronger MBA for Investment Banking, with 28.0% of the Class of 2025 placing into IB at a $175,000 median base, against Booth's 8.3% at the same base.

- Booth is the stronger MBA for Private Equity. Booth placed 5.3% of the Class of 2025 into PE against Stern's 1.3%

- Booth wins for buy-side asset management and quantitative research (Eugene Fama, Richard Thaler, John Cochrane tradition)

- Stern wins for FinTech (David Yermack-led specialization), real estate finance (dual Real Estate Investment and Capital Markets specialization), and the practitioner-facing segments of commercial banking, insurance, and wealth management on

- Both schools place below 2% into Venture Capital

- Q1 2026 Investment Banking trend data points to higher Class of 2026 IB placement at both schools, with Goldman Sachs advisory revenue up 89% year over year and JPMorgan up 82%.

Contents

- The Finance Question in 2026

- Location and the Finance Ecosystem

- Class Profile and Finance Background

- Finance Faculty and Departments

- Curriculum Choice in Finance

- Investment Banking Curriculum

- Private Equity Curriculum

- Diversified Financial Services Curriculum

- Finance Employment Outcomes (Class of 2025)

- Salary Comparison - NYU Stern MBA vs. Chicago Booth MBA

- IB, PE, and VC Industry Trends (Q3 2025 to Q1 2026): What It Means for Booth and Stern Candidates

- Investment Banking: Megadeal Cycle Reopens

- Private Equity: Record Deal Value, Frozen Distributions

- Venture Capital: AI Concentration at 81 Percent

- Verdict for the Finance Applicant - Key Takeaways

- References

The Finance Question in 2026

When MBA applicants ask me which school is better for a finance career, the majority are usually hinting at a school that would be better suited for a buy-side or sell-side role after graduation. The rest want to keep their options open across Consulting, Diversified Financial Services, and Investment Management. The New York vs. Chicago question is only secondary to their inquiry.

The 2025 employment data resolves more of these questions than at any point in the last three years, because finance hiring at the two schools diverged in 2025 along with deal execution.

NYU Stern attracted the Investment Banking talent, while Booth pulled the Diversified Financial Services talent pool[1][2].

Location and the Finance Ecosystem

Booth is based in Hyde Park, on Chicago's South Side, in the Harper Center on the University of Chicago's main campus.

Chicago is the third-largest U.S. metropolitan economy and hosts five derivatives and equity venues, namely CME Group's Chicago Mercantile Exchange and Chicago Board of Trade, Cboe Global Markets, NYSE Chicago, and the Chicago Board Options Exchange floor.

The city also hosts the Federal Reserve Bank of Chicago and around 35 Fortune 500 headquarters, with the headquarters of Citadel, Citadel Securities, and Northern Trust among the top three.

Stern is based in Greenwich Village in Lower Manhattan, four subway stops north of Wall Street and the New York Stock Exchange floor.

The school is within walking distance of NYU Law and the Tisch School, and the same subway line runs to the headquarters of Goldman Sachs, JPMorgan, and Morgan Stanley.

I often profess about access as the single biggest criterion for Investment Banking hiring.

Even though New York hosts more than 45 Fortune 500 headquarters and accounted for over 60% of global investment-banking fee pools during the Q3 2024 to Q2 2025 hiring window for the Class of 2025[2], the proximity that finance candidates enjoy with Stern, and even with Columbia and Cornell to a certain extend should be a priority while choosing schools for an Investment Banking career.

Booth's New York finance recruiting runs through its New York campus and the Booth in New York program, both of which the career services team uses to host on-site IB and PE recruitment.

Nevertheless, IB recruitment at Chicago Booth is still a school-driven initiative and not candidate-driven networking, where most of the opportunities lie.

Regardless of whether the recruitment is driven by the school or the candidate, the recruitment calendar sets out the opportunities available for Booth and Stern MBA candidates.

Stern students can take a 30-minute lunch break at a bulge-bracket office, whereas Booth students rely on bank fly-ins, school-organized treks to New York, and on-campus interviews in the Harper Center.

As candidates take on multiple interview rounds, Employers have an implicit bias in favor of students who can do superdays in person without missing class.

NYU Stern beats Booth in that regard.

Class Profile and Finance Background

Chicago Booth's Full-time MBA Class of 2027 constitutes 635 matriculants. The women and international student representation were within the 40-45% range for women with 41% women, and 30-40% international range, with 37% international students.

The pre-MBA industry mix is 23% Consulting, 22% Financial Services, 12% Nonprofit and Government, 10% Technology, and 8% Private Equity or Venture Capital, with the remainder spread across Healthcare, Energy, and Consumer Products[6].

The previous class, Class of 2026, was 632 matriculants from 5,125 applicants, also had a similar distribution where Consulting and Finance candidates were hired on equal footing, while non-profit and government overtook the Technology and PE/VC cohort[6].

Stern's Full-time Two-Year MBA program enrolls a smaller class than Booth, in the high 300s, with finance professionals making up over 20% of the class profile before matriculation[2]. The consulting and finance distribution is not equal at Stern. A large percentage of consulting entrants are from career switchers, contributing to the allure of NYU Stern. The per-student attention that the career services team offers and a denser finance sub-industry alumni concentration in New York are two other contributing factors for the strong Finance placements at NYU Stern.

Booth's larger class produces a broader on-campus employer set - 170 unique companies for the Class of 2025, and an 89% rate of graduates accepting offers within three months of graduation[5].

Finance Faculty and Departments

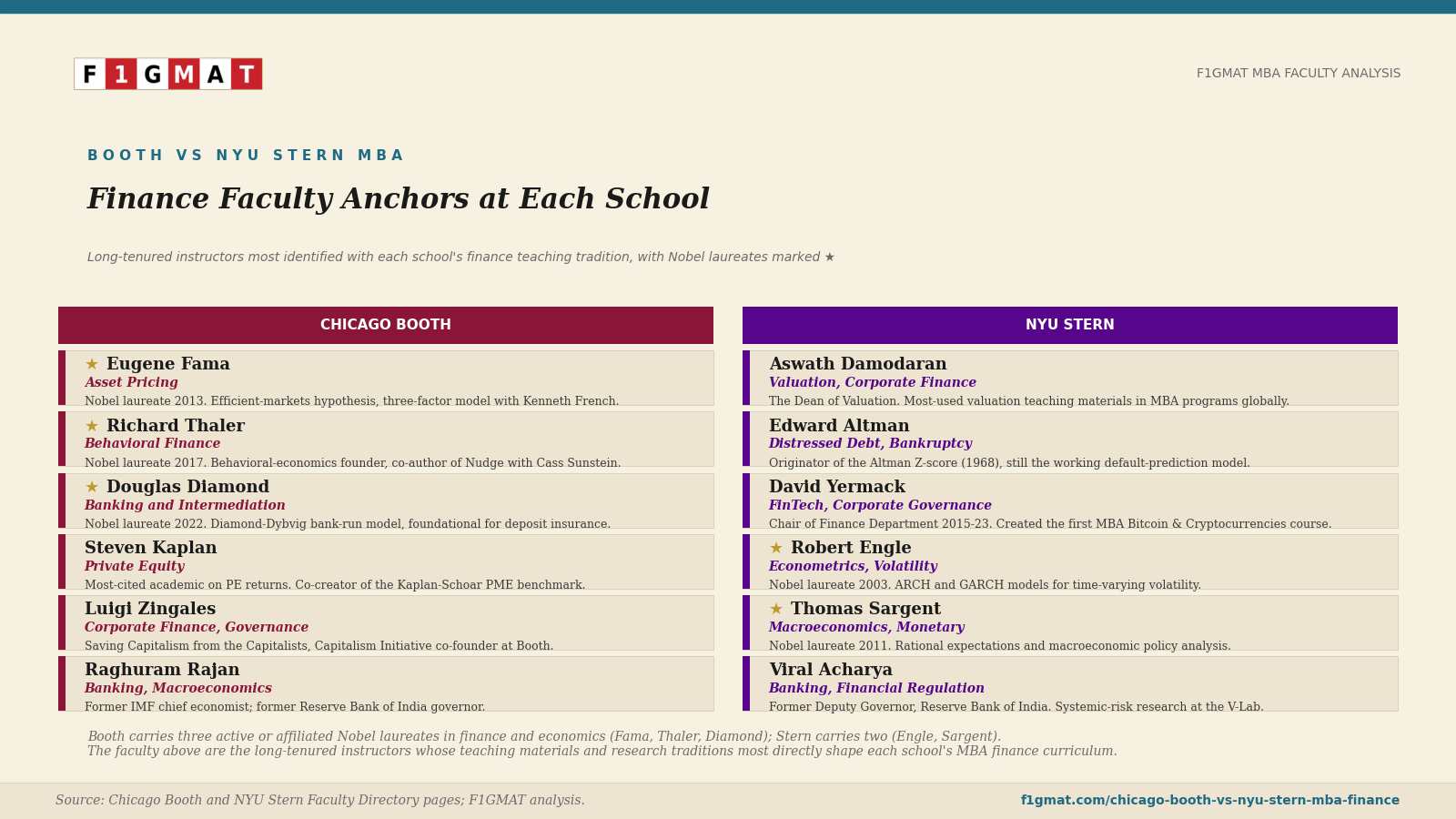

Booth's finance reputation rests on the University of Chicago Department of Economics and Booth's own Finance group, both of which originated foundational frameworks in modern finance.

Eugene Fama on efficient markets and asset pricing, Lars Peter Hansen on generalized method of moments, Myron Scholes on options pricing, and Richard Thaler on behavioral finance.

Eugene F. Fama is best known for developing the Efficient Market Hypothesis[11], which states that assets are priced in based on all the information available, making it extremely difficult to consistently outperform the market on a risk-adjusted basis. Fama's research laid the foundation for modern empirical asset pricing and portfolio theory. The research won him the 2013 Nobel Prize in Economics, which he shared with Lars Peter Hansen and Robert Shiller.

Lars Peter Hansen created the Generalized Method of Moments (GMM)[12], a powerful statistical technique that estimates economic models using moment conditions. This method provides robust tools for testing asset pricing theories and handling complex issues such as endogeneity in financial and macroeconomic data without requiring the full probability distribution of the data. His framework has become a standard tool in empirical research across economics and finance. Hansen was awarded the 2013 Nobel Prize in Economics together with Eugene Fama and Robert Shiller.

Outside the accolades Booth professors Eugene Fama and Lars Peter Hansen earned in one Nobel year, Myron Scholes was considered the pioneer who set the Booth brand on a global platform. He co-developed the Black-Scholes model[13], which provides a mathematical formula for pricing options based on no-arbitrage principles and risk-neutral valuation. The model shows how option prices depend on factors like the underlying asset price, strike price, volatility, time to expiration, and the risk-free rate. This breakthrough fundamentally transformed derivatives markets and enabled the rapid growth of options trading worldwide. Scholes received the 1997 Nobel Prize in Economics, which he shared with Robert Merton.

Richard Thaler[14] is the outlier among the recent Booth professors. His pioneering work integrated insights from psychology into economic theory. According to him, many market anomalies cannot be accounted for based on traditional rational models as investors employ loss aversion and mental accounting in their financial decisions.

By introducing the concept of nudges to influence better choices, Thaler has shaped public policy strategies through his research. He was awarded the 2017 Nobel Prize in Economics for his contributions to behavioral economics.

Chicago Booth has produced more Nobel laureates in Economics than any other institution.

With nine laureates affiliated through Booth alone, the legacy adds to the allure of the Booth brand and reinforces a culture of data, econometrics, and decision frameworks, which Booth has pioneered.

Stern's Department of Finance, chaired by faculty including Aswath Damodaran on valuation, Edward Altman on credit risk (the Altman Z-score), and Robert Whitelaw on derivatives, runs one of the largest faculty groups in the U.S. covering corporate finance, asset pricing, fintech, fixed income, and financial econometrics.

Aswath Damodaran[15] is one of the world's leading authorities on valuation, corporate finance, and investment philosophy. He has developed comprehensive frameworks for valuing companies, including techniques for young growth firms, distressed businesses, and firms in emerging markets.

Edward Altman[16] would be more renowned for Finance applicants, as the creator of the Altman Z-score, a widely adopted statistical model that uses financial ratios to predict the probability of corporate bankruptcy. Altman's research is widely used for credit risk analysis for banks, investors, and rating agencies, and expands to non-manufacturing firms, emerging markets, and distressed debt investing.

Robert Whitelaw[17] is an expert in derivatives, asset pricing, fixed income, and risk management. His research explores the pricing and hedging of financial instruments, volatility, and the behavior of stock and bond markets, including work on China's financial system. He serves as the Edward C. Johnson III Professor of Entrepreneurial Finance at NYU Stern School of Business.

Even though the professor's pedigree is not as comparable as Booth’s, NYU Stern offers a breadth of finance electives and the practitioners from Wall Street who frequently join in adjunct teaching roles, which Booth cannot replicate by geography.

On the Finance Ph.D. and academic recruiting front, Booth has the edge in academic publication output and Nobel-grade name recognition.

On the practitioner-driven finance electives front, Stern has the edge in volume and recency of New York case material.

Neither edge is decisive for the average finance MBA who plans to work in IB, PE, or asset management.

Both edges matter for the candidate who plans to go into quant research, investment management, or academia.

Curriculum Choice in Finance

Booth students choose 11 electives from roughly 130 courses across 13 concentrations, of which Finance, Analytic Finance, Accounting, Econometrics and Statistics, Economics, and Entrepreneurship are the six concentrations finance candidates most often combine.

Booth's Analytic Finance concentration carries a STEM designation, which gives international students 36 months of OPT (Optional Practical Training, a U.S. work-authorization extension for STEM graduates) instead of the standard 12 months[10].

Stern offers more than 300 electives, with the Department of Finance accounting for roughly 70 of them.

The school has 24 specializations, nine of which are finance-related: Finance, Financial Instruments and Markets, Financial Systems and Analytics, FinTech, Quantitative Finance, Banking, Corporate Finance, Investments, and Real Estate. Stern's MBA is STEM-designated as a whole through the Technology, Operations, and Statistics concentration.

Stern requires more core courses than Booth (two mandatory finance and accounting cores plus a selection of additional core electives), so the practical elective bandwidth is narrower than Booth's, even though the total elective catalog is larger[10].

Choosing between the two curricula starts with knowing which post-MBA finance role the candidate is preparing for.

The three subsections below cluster around the questions candidates ask most often - which school is ideal for Investment Banking, which one for Private Equity, and which one for the broader Diversified Financial Services category.

The verdict at the end of each cluster identifies which school's curriculum offers stronger preparation. For the full role-by-role course mapping and the split verdicts based on the quality of the course and professor, subscribe and read from F1GMAT Premium.

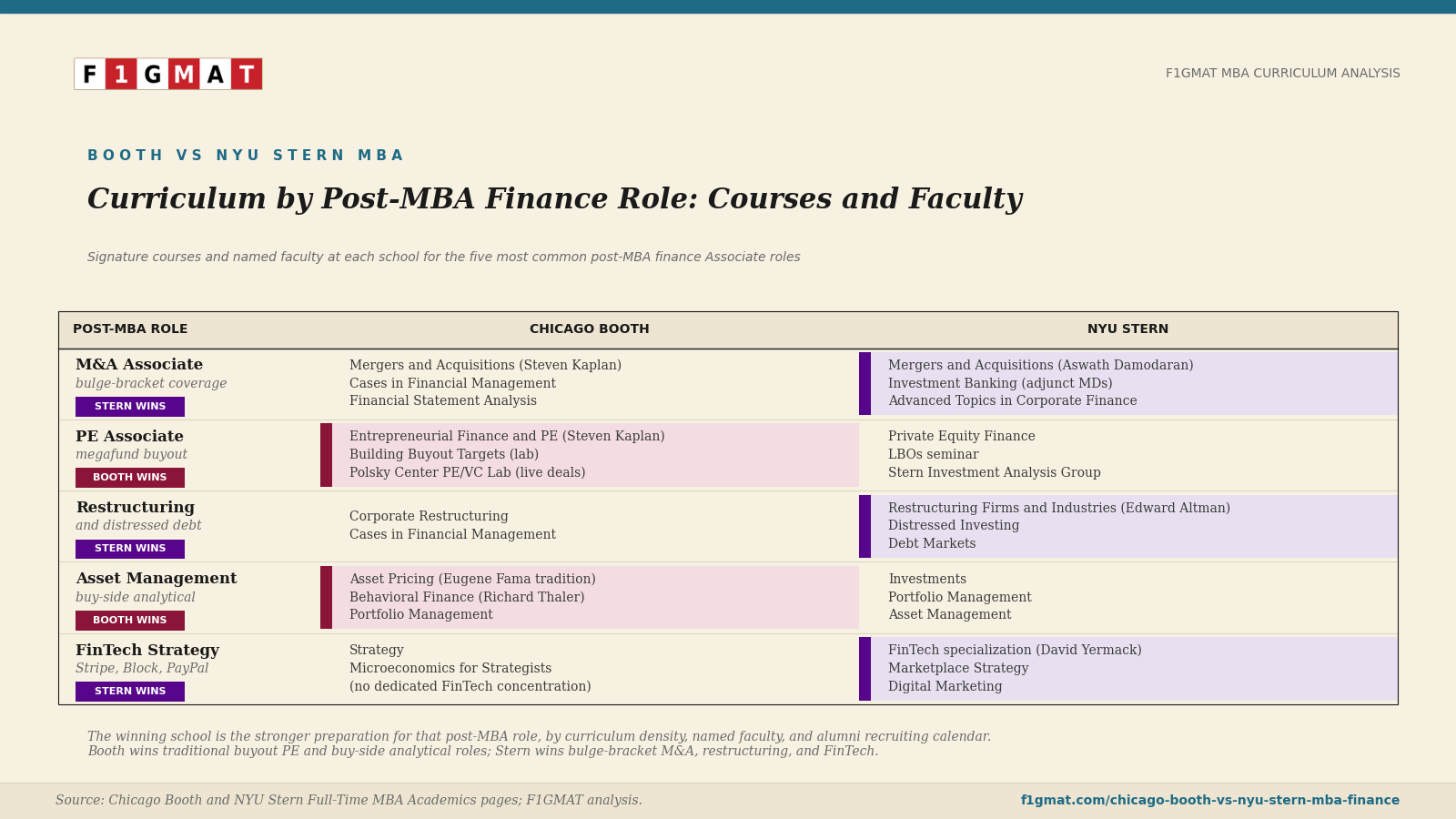

Investment Banking Curriculum

A strong investment banking curriculum must be built on a strong foundation in Corporate Finance and Valuation.

Post-MBA associate roles in Investment Banking depend on the specialization.

M&A coverage, Leveraged Finance, Equity Capital Markets, Debt Capital Markets, and Restructuring - each require different set of electives.

The two schools differ less on the foundation and more on the specialized layer above it, which is where curriculum design and faculty's expertise offer different values for a NYU Stern MBA and a Chicago Booth MBA candidate.

Which MBA program is better for investment banking, Chicago Booth or NYU Stern?

NYU Stern is the stronger MBA program for Investment Banking, with 28.0% of the Class of 2025 placing into IB against Chicago Booth's 8.3%[1][2]. The gap reflects Stern's New York campus, the bulge-bracket on-campus recruiting calendar, and a dedicated Investment Banking course taught by active managing directors.

Booth remains competitive for candidates targeting boutiques such as Evercore, Centerview, Lazard, and PJT Partners.

Who teaches M&A at NYU Stern and at Chicago Booth?

Aswath Damodaran teaches the M&A course at NYU Stern, and Steven Kaplan teaches the M&A course at Chicago Booth.

Damodaran's valuation lectures are the most-used finance teaching materials globally. Kaplan is the most-cited academic on private equity returns and LBO economics, and his research informs his M&A course design.

The two professors approach the same body of material from opposite ends.

Damodaran builds the deal model up from intrinsic valuation, with a working assumption that the candidate will spend the next decade pricing public companies and arguing about discount rates. The course design favors the sell-side Associate who needs to defend a fairness opinion in front of a board.

Kaplan builds the deal model down from the sponsor's return on equity, with a working assumption that the candidate will spend the next decade running an LBO model under multiple capital structures. The course design favors the boutique Associate working sponsor-coverage deals at Evercore or Centerview.

Does NYU Stern have a dedicated Investment Banking course?

Stern offers a dedicated Investment Banking course taught by adjunct faculty who currently serve as managing directors in IB firms. Booth does not offer a direct equivalent, though its M&A and Corporate Restructuring electives cover overlapping deal-execution material. The Stern course relies on Manhattan's bulge-bracket cases, which Chicago's smaller bank presence cannot match.

How do MBA programs prepare candidates for restructuring and distressed-debt roles?

NYU Stern's Edward Altman built the Z-score model for default prediction in 1968, and Stern's Restructuring Firms and Industries and Distressed Investing courses are based on that research foundation.

Booth's Corporate Restructuring course covers the same Chapter 11 (the U.S. corporate reorganization process) material from a corporate-finance perspective.

For a candidate targeting Houlihan Lokey, PJT Restructuring, or Lazard's restructuring group, Stern's faculty depth is a better option.

The Class of 2025 placement data show the subtle strengths.

Stern's 28.0% IB share concentrates in M&A coverage groups at the bulge brackets, where Damodaran's valuation framework and the dedicated IB course produce candidates who are calendar-ready by January of the second year.

Booth's 8.3% IB share concentrates in boutique M&A and sponsor coverage, where the Kaplan-Vishny corporate-finance tradition matches the seat.

Q1 2026 IB earnings data, with advisory revenue rising 89% year over year at Goldman Sachs and 82% at JPMorgan[7], suggests that the Class of 2026 IB share will run higher at both schools.

| IB Associate role | Which school wins, and why in one phrase |

|---|---|

| M&A Associate (TMT, Healthcare, Industrials, FIG coverage) | Stern, on Damodaran's Valuation course and the bulge-bracket calendar |

| Leveraged Finance Associate | Tied: Booth's Kaplan PE for the sponsor side; Stern's Debt Markets for coverage |

| Equity Capital Markets Associate | Stern, on syndicate-desk proximity in New York |

| Debt Capital Markets Associate | Stern, on Debt Markets and Fixed Income depth |

| Restructuring Associate | Stern, on Altman's Z-score research foundation |

The full five-role IB course map with the specific Booth and Stern courses for each Associate variant, the named faculty per course, the boutique-versus-bulge-bracket split verdict, and a course-sequencing plan by quarter is in F1GMAT Premium.

Private Equity Curriculum

A strong PE Curriculum depends on the post-MBA role you are targeting.

The roles can be broadly classified under 5 buckets - traditional buyout at a megafund or middle-market firm, growth equity, operating roles inside portfolio companies, private credit (direct lending, mezzanine, or distressed), and fund-of-funds or GP (general partner) selection.

Each path uses a different mix of valuation, modeling, operations, and credit electives, and the curriculum gap between Booth and Stern is wider in PE than in any other finance category.

Which MBA program is better for private equity, Chicago Booth or NYU Stern?

Chicago Booth is the stronger MBA program for Private Equity, with 5.3% of the Class of 2025 placing into PE against NYU Stern's 1.3%[1][2]. Booth's edge runs through Steven Kaplan, the most-cited academic on PE returns and LBO economics, his canonical Entrepreneurial Finance and Private Equity course, and the Polsky Center Private Equity and Venture Capital Lab, where students execute live diligence on real Chicago-area transactions. The Chicago megafund alumni network at KKR, Carlyle, Madison Dearborn, and GTCR compounds the curriculum advantage.

Who teaches private equity at Chicago Booth?

Steven Kaplan[18] teaches Entrepreneurial Finance and Private Equity at Chicago Booth, the canonical academic PE course in U.S. MBA programs for two decades. Kaplan's research on PE returns, fund performance persistence, and LBO economics is the most-cited body of academic work in the industry. His course pairs with the Polsky Center Private Equity and Venture Capital Lab as Booth's experiential PE elective.

Kaplan's academic influence runs deeper through his research on LBO capital structures. Students learn to identify leverage tolerance in mega funds.

A Booth graduate enters a PE role with the working vocabulary that Kaplan's research established, which compounds the recruiting advantage.

Stern's PE curriculum is smaller in absolute course count and does not have an equivalent superstar faculty, though the school's Distressed Investing track gives it a different kind of edge on the credit side.

What is the Polsky Center Private Equity and Venture Capital Lab?

The Polsky Center Private Equity and Venture Capital Lab[10] is a Chicago Booth elective in which students execute live diligence on real PE and VC transactions with Chicago-area investment firms during the academic year. The course is administered through the Polsky Center for Entrepreneurship and Innovation. NYU Stern does not offer an equivalent live-deal lab.

Which MBA is better for private credit or distressed debt?

NYU Stern is the stronger MBA for private credit and distressed debt, on the foundation of Edward Altman's research and the school's Distressed Investing and Restructuring Firms and Industries courses. Booth's Corporate Restructuring covers similar material but without the same faculty depth.

The Q1 2026 trend of opportunistic credit fundraising surpassing direct lending for the first time, anchored by Goldman Sachs at $13 billion in mezzanine and Benefit Street at $10 billion in commercial real estate[8], makes Stern's distressed track more useful in the current cycle than at any point in the last five years.

What MBA courses prepare a candidate for a growth equity Associate role?

Chicago Booth's Entrepreneurial Finance and Private Equity (Kaplan), New Venture Strategy, and Microeconomics for Strategists courses prepare candidates for growth equity at firms such as General Atlantic, TA Associates, and Summit Partners.

NYU Stern's Entrepreneurial Finance and Private Equity Finance cover the same ground from a New York-employer angle. The FinTech specialization adds depth for growth equity in fintech (Stripe, Block, Klarna). Growth equity hires draw from both schools in roughly equal numbers because the role rewards founder empathy and operator instinct as much as pure LBO modeling.

The PE placement gap (5.3% Booth, 1.3% Stern) is paradoxical against a record PE deal year. Q1 2026 produced 5,100 transactions worth $481.6 billion, $2 trillion in global dry powder, and 22 megadeals at or above $10 billion in a single quarter, a record[8]. The reason placements stayed in single digits at both schools is that the megafunds routed Associate hiring through pre-MBA two-year analyst pipelines and held off on rebuilding post-MBA volume. Booth's curriculum advantage will matter more for the Class of 2027 when the 11,000 portfolio companies held longer than five years come up for exit and the megafunds reopen post-MBA classes to clear deal backlog.

| PE Associate role | Which school wins |

|---|---|

| Buyout Associate (megafund or middle-market) | Booth, on Kaplan's Entrepreneurial Finance and Private Equity course and the Polsky PE/VC Lab |

| Growth Equity Associate | Booth, on the Kaplan course extended with New Venture Strategy |

| Operating Associate (portfolio operations) | Tied: both schools offer Operations Management and strategy electives |

| Private Credit Associate (direct lending, mezzanine, distressed) | Stern, on Altman's Distressed Investing and Restructuring Firms and Industries |

| Fund-of-Funds / GP Selection Associate | Booth, on Fama's Asset Pricing tradition and Advanced Investments |

The full five-role PE course map with named faculty per course, the traditional-buyout-versus-private-credit split verdict, the course-sequencing plan for a megafund-target candidate at each school, and the Q1 2026 trend implications for Class of 2027 PE recruiting is in F1GMAT Premium. Read on F1GMAT Premium

Diversified Financial Services Curriculum

Diversified Financial Services (DFS) is the broadest of the three finance categories.

Booth reports 9.0% of its Class of 2025 into DFS at $215,000 total compensation[1], a figure that aggregates six distinct role types under one label. Stern does not break this category out separately in its employment report.

The six DFS Associate roles use different curriculum stacks, and Booth and Stern split the wins across them in roughly equal halves.

What does Diversified Financial Services mean as an MBA employment category?

Diversified Financial Services (DFS) is the MBA employment category that aggregates six finance roles: asset management, commercial banking, insurance, FinTech, wealth management, and real estate finance.

Chicago Booth reports 9.0% of its Class of 2025 placing into this category at $215,000 total compensation[1].

NYU Stern does not break this category out separately in its employment report, instead reporting individual sub-segments inside Financial Services.

Which MBA is better for asset management and buy-side analytical roles?

Chicago Booth is the stronger MBA for asset management and buy-side analytical roles, on the foundation of Eugene Fama (Nobel laureate in economics for his work on efficient markets), Richard Thaler (Nobel laureate for behavioral economics), and John Cochrane (asset pricing and macroeconomics).

The Booth Asset Pricing, Behavioral Finance, and Portfolio Management electives are based on this faculty tradition. A candidate targeting BlackRock factor research, AQR systematic strategies, or a quant pod at Citadel or Millennium should pick Booth on curriculum strength alone.

The DFS category is where the curriculum gap between the two schools is the widest in finance-specific specializations.

Booth concentrates its DFS strength on the buy-side analytical end, where the Fama-Thaler-Cochrane academic tradition produced the asset-pricing and behavioral frameworks that hedge funds and asset managers use as standard vocabulary.

Stern concentrates its DFS strength on the practitioner-facing end, where specialization signaling on the resume and proximity to New York employers both work together.

Which MBA is better for FinTech?

NYU Stern is the stronger MBA for FinTech.

A dedicated FinTech specialization is offered under the faculty leadership of David Yermack, who has helped shape the curriculum since 2016, which includes courses on Bitcoin & Cryptocurrencies, blockchain, and related topics that he personally teaches (often jointly with NYU Law).

Chicago Booth does not offer a comparable FinTech concentration or the exposure that New York offers, though there are targeted electives like The FinTech Revolution, which covers blockchain, virtual currencies, smart contracts, opportunities, challenges, and regulatory issues, and Decoding FinTech, which is a high-level overview of Blockchain and AI.

The Stern FinTech specialization matters most for candidates targeting product and strategy roles at Stripe, Block, PayPal, Klarna, and Affirm.

Which MBA is better for real estate finance?

NYU Stern is the stronger MBA for real estate finance. With both Real Estate Investment and Real Estate Capital Markets as published specializations, Stern has the depth that Chicago Booth doesn't match with a single Real Estate Investments course.

Stern's curriculum is designed to support candidates targeting REITs (Blackstone Mortgage Trust, Starwood Property Trust), real estate private equity (Blackstone Real Estate, Brookfield), and real estate banking groups inside JPMorgan, Wells Fargo, and Bank of America.

Which MBA is better for commercial banking, insurance, and wealth management?

NYU Stern is the stronger MBA for commercial banking, insurance, and wealth management, on the foundation of New York’s employer density. JPMorgan, Wells Fargo, and Citi corporate banking concentrate their MBA hiring around Stern's calendar. MetLife, Prudential, and AIG run their insurance graduate programs from New York. Morgan Stanley PWM, Goldman PWM, and JPM Private Bank pull from Stern at materially higher rates than Booth because the wealth management seat is geographically concentrated.

The Financial Services verdict is split.

Booth wins for buy-side asset management, insurance asset-liability work, and quantitative research, where the Fama-Thaler-Cochrane academic tradition produced the frameworks the buy-side actually uses.

Stern wins the FinTech, real estate finance, commercial banking, insurance underwriting, and wealth management niches, where curriculum specialization and New York's employer concentration offer Stern an advantage.

The choice within DFS collapses to the choice of role, not the choice of school.

| Diversified Financial Services Associate role | Which school wins? |

|---|---|

| Asset Management Analyst (BlackRock, JPM Asset Management, T. Rowe Price) | Booth, on Fama's Asset Pricing and Thaler's Behavioral Finance |

| Corporate / Commercial Banking Associate | Stern, on New York employer density at JPMorgan, Wells Fargo, and Citi |

| Insurance Company Analyst (MetLife, Prudential, AIG) | Stern, on the dedicated Insurance specialization and New York employer concentration |

| FinTech Strategy Associate (Stripe, Block, PayPal, Klarna, Affirm) | Stern, on the Yermack-led FinTech specialization |

| Wealth Management / Private Banking Associate | Stern, on New York private-bank concentration at Morgan Stanley PWM, Goldman PWM, and JPM Private Bank |

| Real Estate Finance Associate (REITs, real estate PE, real estate banking) | Stern, on the dual Real Estate Investment and Real Estate Capital Markets specialization |

The full six-role DFS course map, the buy-side-analytical-versus-practitioner-facing split verdict, the role-specific course sequence for a BlackRock factor-research role at Booth and a Stripe product-strategy role at Stern, and the Q1 2026 trend implications (GENIUS Act stablecoin charters, AI capture of 81% of venture funding) for FinTech and asset-management hiring are in F1GMAT Premium.

Final Verdict - NYU Stern vs. Chicago Booth MBA Curriculum

The overall curriculum verdict tracks the three subsection verdicts.

NYU Stern is the stronger preparation for Investment Banking, for FinTech, for real estate finance, and for the practitioner-facing DFS segments (commercial banking, insurance, wealth management).

Chicago Booth is the stronger preparation for Private Equity (specifically traditional buyout and growth equity), for the buy-side analytical DFS segments (asset management, quantitative research), and for the boutique end of M&A coverage. The choice between the two curricula collapses to the choice between two specific post-MBA Associate seats, not the choice between two general MBA programs.

The full Section 5 (with the role-by-role responsibility-and-course mapping for all sixteen Associate roles across the three industries, the split verdicts inside each industry, the per-school course sequencing plans for the highest-demand seats, and the Q1 2026 trend-data cross-references that translate the cycle into specific elective decisions) is available to F1GMAT Premium subscribers.

Finance Employment Outcomes (Class of 2025)

Both reports cover the Class of 2025 graduating class, with the recruitment window spanning Q3 2024 through Q2 2025[3][4].

This was a time when IB hadn’t fully recovered, and deal sizes hadn’t picked up to the astronomical scale that we saw in 2025 Q4 and Q1 2026.

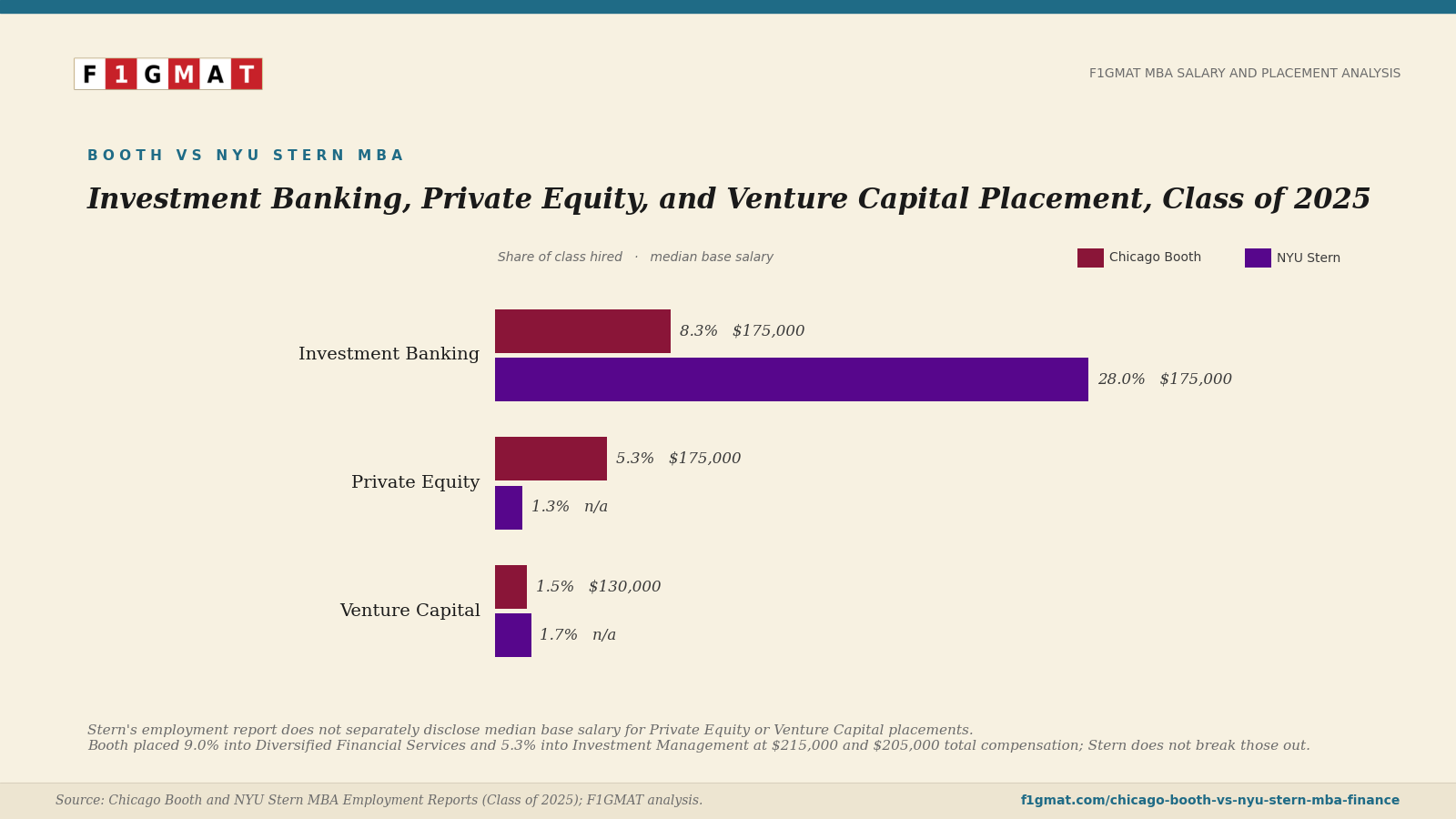

| Industry / Sub-industry | Booth (Class of 2025) | NYU Stern (Class of 2025) |

|---|---|---|

| Consulting | 36.7% · $190,000 base | 32.8% · $175,000 base |

| Financial Services (all) | 31.6% · $175,000 base | 36.6% · $175,000 base |

| Investment Banking | 8.3% · $175,000 base · $50,000 sign-on | 28.0% · $175,000 base · $57,448 avg sign-on |

| Diversified Financial Services | 9.0% · $175,000 base · $40,000 sign-on | Not separately broken out |

| Investment Management / Research | 5.3% · $165,000 base · $40,000 sign-on | Not separately broken out |

| Private Equity | 5.3% · $175,000 base · bonus n/a | 1.3% · bonus n/a |

| Venture Capital | 1.5% · $130,000 base | 1.7% · bonus n/a |

| Technology | 14.1% · $151,000 base | 14.2% · $152,500 base |

| Healthcare / Pharma / Biotech | 4.1% · $145,000 base | 3.4% · $138,500 base |

| Law | 4.5% · $225,000 base | 3.4% · $235,000 base |

Source: F1GMAT industry analyses of the Class of 2025 employment reports for Chicago Booth and NYU Stern. Bonus figures: Booth reports median sign-on; Stern reports average signing bonus.

Investment Banking

Investment Banking is the single largest divergence between the two schools.

Stern placed 28.0% of the Class of 2025 into Investment Banking at a $175,000 median base and a $57,448 average signing bonus, the highest signing bonus among all major industries[2].

Booth placed 8.3% of the Class of 2025 into Investment Banking and Brokerage at the same $175,000 median base, a $50,000 median sign-on, and a $225,000 total compensation figure that is the highest median total across Booth's industries[1].

The gap between 28% and 8.3% is not a difference in quality of IB hire, since the base salaries match at $175,000, and the bonuses are within $10,000 of each other.

The gap is a difference in volume of IB hires, driven by Stern's New York location and the school's brand among bulge-bracket and elite-boutique IB recruiters.

Stern saw Investment Banking hiring rebound from the 2022 to 2023 levels, although base salaries stayed flat and bonuses expanded [2]. Booth saw IB hiring contract from a 2023 peak of 11.1% to 9.4% in 2024 and 8.3% in 2025, a gradual pullback that tracks the broader market preference for lateral over MBA hiring during the same window[1].

For a candidate whose post-MBA goal is Investment Banking specifically, Stern is the higher-probability bet, by a wide margin. For a candidate whose Investment Banking interest is one of several finance paths, Booth's 8.3% understates the school's IB pipeline because Booth captures a different mix of finance candidates into Diversified Financial Services and Investment Management instead.

Diversified Financial Services

Diversified Financial Services is the Booth speciality Stern does not report separately - a clear signal on where Booth's strength lies.

Booth placed 9.0% of the Class of 2025 into Diversified Financial Services at a $175,000 median base, a $40,000 median sign-on, and a $215,000 total compensation, which puts the category on near-equal compensation footing with Investment Banking at Booth[1].

The category covers fintech infrastructure, corporate finance roles at non-bank financial institutions, asset servicing, payments, risk platforms, and financial analytics. The 9.0% share is the result of a multi-year expansion. The category was between 6% and 7% from 2021 to 2023, jumped to 11.4% in 2024, and held at 9.0% in 2025[1].

The applicant takeaway is that Booth's finance pipeline is wider than the Investment Banking headline implies.

Adding Investment Banking, Diversified Financial Services, and Investment Management together, Booth placed 22.6% of the Class of 2025 into core finance sub-industries that compete with Stern's IB-heavy mix.

Stern reports Investment Banking, Private Equity, and Venture Capital, so the like-for-like Stern aggregate is 31.0% (28.0 + 1.3 + 1.7).

Booth's full Financial Services category represents 31.6%, which is almost identical to Stern's 36.6% once Booth's Diversified Financial Services is included.

Private Equity

Private Equity is the weakest segment at both schools.

The gap between them is small.

Booth placed 5.3% of the Class of 2025 into Private Equity at a $175,000 median base, with bonus and total compensation not reported by the school, a data omission that F1GMAT's analysis flags as a negative signal for PE outcomes[1].

Booth's PE share fell from 6.4% in 2024 and from a 2023 peak of 9.1%.

Stern placed 1.3% into Private Equity, with compensation not reported because the sample size is below the school's disclosure threshold[2].

The 5.3% versus 1.3% placements in PE might be misinterpreted as an advantage for Booth.

If you look back at the recruitment cycle, PE firms did not rebuild MBA-associate benches between Q3 2024 and Q2 2025. The capital allocation was planned for AI investments. The firms instead relied on pre-MBA analyst pipelines, lateral hiring, and operating-partner models.

F1GMAT's analysis attributes the low PE conversion at Stern, despite Stern's large finance-background class, to the fact that PE recovery in this cycle was driven by tariff-war complexity, private credit, and IPO-adjacent expertise that finance-heavy MBA pools did not natively offer[2].

For a candidate whose post-MBA target is mid-market or megafund PE, neither school is a reliable placement engine.

Pre-MBA PE or banking experience and a sponsor-side network matter more than the school choice.

Venture Capital

Booth placed 1.5% of the Class of 2025 into VC at a $130,000 median base[1] while Stern placed 1.7%, with compensation not separately disclosed[2] - a signal that Stern has low representation and marginal compensation to report as a separate entry.

Both reflect the same external dynamic - VC capital concentrated in AI infrastructure and late-stage platforms during the recruitment window. Hiring for the junior MBA-track roles has paused across the venture capital industry.

Chicago VC fundraising was at a seven-year low during this period, which F1GMAT's analysis cites as the proximate reason for Booth's $130,000 VC median base, well below the school's finance median[1].

Investment Management and Research

Investment Management was an underperformer at Booth, with 5.3% of the Class of 2025 entering Investment Management and Research at a $165,000 median base, a $40,000 sign-on, and $205,000 total compensation, which is below Booth's broader finance median[1]. This is a contrarian trend to M7 compensation in Investment Management.

F1GMAT's analysis attributes the lower compensation to the asset management industry's shift toward AI-driven research tools, systematic strategies, and risk-overlay models, which reduced the volume of generalist analyst intakes between Q4 2024 and Q2 2025 and pushed Investment Management MBA hires into more technical, quantitatively anchored roles[1].

Stern does not break Investment Management out from Financial Services in its 2025 report, which makes a like-for-like comparison difficult.

The aggregate Stern Financial Services average signing bonus of $56,657 is above Booth's Investment Management $40,000 sign-on, which suggests Stern's Investment Management roles, whatever their share, attract higher New York buy-side bonus structures than Booth's Chicago-weighted asset management pipeline[2].

Salary Comparison - NYU Stern MBA vs. Chicago Booth MBA

Booth's Class of 2025 median base salary across Financial Services placements was $175,000. A $45,000 median sign-on takes the total to $220,000 [1] [3]. Stern's Class of 2025 Financial Services, on the other hand, also had the same $175,000 base salary for 36.6% of the class, with a higher $56,657 average signing bonus that reflects the Investment Banking weight inside Stern's Financial Services category [2].

The 2025 reports show that base salary parity continues, while New York signing bonuses run roughly $7,000 to $12,000 higher than Chicago equivalents[1][2].

Note on Salary Comparison: Booth publishes medians and breaks out sub-industries within Financial Services; Stern publishes medians plus averages for signing bonuses and groups smaller sub-industries under Financial Services without separate breakouts for Diversified Financial Services, Investment Management, or Corporate Finance roles.

| School (Class of 2025) | Industry % | F1GMAT analysis link |

|---|---|---|

| Wharton — Industry analysis | Finance and Consulting dominant | Wharton 2025 industry |

| Columbia — Industry analysis | Finance leader in NY peer set | Columbia 2025 industry |

| Kellogg — Industry analysis | Consulting-led, finance secondary | Kellogg 2025 industry |

| MIT Sloan — Industry analysis | Tech-led, finance secondary | MIT Sloan 2025 industry |

| Booth — Industry analysis | Consulting 36.7%, Finance 31.6% | Booth 2025 industry |

| NYU Stern — Industry analysis | Finance 36.6%, Consulting 32.8% | Stern 2025 industry |

All analyses linked above are F1GMAT publications of the relevant school's Class of 2025 employment data. Full index available at the F1GMAT MBA Salary page.

IB, PE, and VC Industry Trends (Q3 2025 to Q1 2026): What It Means for Booth and Stern Candidates

The 2025 placement numbers Booth and Stern reported are an output of what investment banks, private equity firms, and venture funds were doing during the same recruiting cycle.

The three subsections below trace the Investment Banking, Private Equity, and Venture Capital trend lines from Q3 2025 through Q1 2026, using F1GMAT Premium's quarterly trend reviews[7][8][9], and connect each trend to what a Booth or Stern candidate should expect from the next two recruiting seasons.

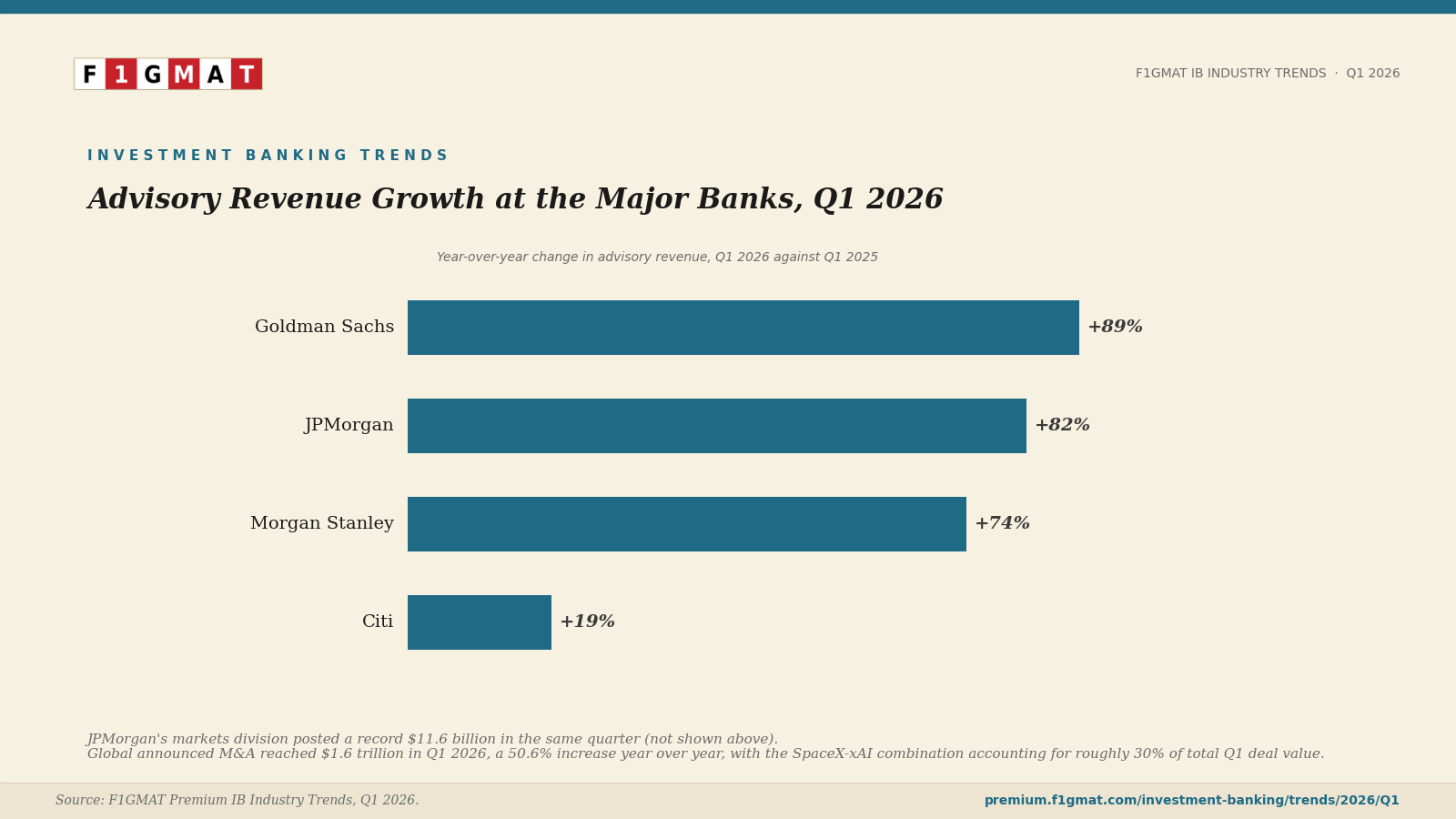

Investment Banking: Megadeal Cycle Reopens

In Q3 2025, M&A advisory ran on a small number of very large transactions.

Global announced deal value crossed $1 trillion (+40% year over year), but the count of total transactions touched a two-decade low, with a record number of deals at or above $10 billion.

The quarter's signature deal was the $55 billion take-private of Electronic Arts by Silver Lake, Saudi Arabia's Public Investment Fund, and Affinity Partners. Sales and trading earnings hit multi-year highs (Citi's fixed income, currencies, and commodities desk crossed $4 billion for the first time), Healthcare M&A doubled quarter on quarter to about $70.5 billion, and the U.S. IPO market posted its strongest quarter since Q4 2021[7].

In Q4 2025, the megadeal cycle accelerated.

Full-year 2025 global M&A value reached $4.3 trillion (+40% year over year), and the count of deals at or above $10 billion rose 128% year over year. The United States captured roughly half of the global value and about 60% of the total M&A activity. The GENIUS Act, the federal stablecoin framework signed into law during the quarter, opened a new product line for the banks' digital asset desks[7].

The momentum continued in Q1 2026, when IB earnings posted their strongest quarter since 2015.

Global M&A reached $1.6 trillion (+50.6% year over year, a record), although total deal count fell about 30%, with the SpaceX-xAI combination accounting for roughly 30% of total Q1 value.

Paramount's $110 billion merger with Warner Bros. Discovery was the largest media merger ever announced, with Bank of America, Citi, Centerview, and LionTree advising the buy side and JPMorgan, Allen & Company, and Evercore advising the sell side.

Advisory revenue rose 89% year over year at Goldman Sachs, 82% at JPMorgan, 74% at Morgan Stanley, and 19% at Citi, with JPMorgan's markets division posting a record $11.6 billion.

Equity capital markets posted its best Q1 in five years ($9.4 billion across 22 IPOs, $31 billion in convertibles, $35 billion in follow-on offerings).

The Federal Reserve re-proposed Basel III, a re-proposal that lowers aggregate bank capital requirements by about 6%[7].

Implications for Booth and Stern candidates

Stern's 28.0% Investment Banking placement and Booth's 8.3% placement[1][2] were set during the Q3 to Q4 2025 recruiting cycle, the same months in which the major banks were posting their strongest advisory quarters in nearly a decade.

Stern's New York campus puts its candidates inside the calendar of the banks whose advisory fees just rose 80% year over year, and the buy-side and sell-side advisor seats on Paramount-Warner Bros. Discovery and SpaceX-xAI sit in the same office towers where Stern runs its career programming.

For Booth IB candidates, the same trend favors them at boutiques that gained advisory share (Evercore, Centerview, Lazard, PJT Partners).

Class of 2026 IB placements should be stronger at both schools if the Q1 2026 fee trajectory continues into the fall recruiting cycle.

Private Equity: Record Deal Value, Frozen Distributions

In Q3 2025, private equity posted a record deal value of about $537 billion globally, with the United States alone accounting for over $300 billion.

Six transactions cleared $10 billion, equal to the count for the entire first half of the year, where the Electronic Arts buyout had a clear impact on the total deal value.

Distribution to paid-in capital, the cash funds return to investors, became the operative metric, and global PE exit value rose 40% year to date to $470 billion.

PE-backed IPOs raised more than $18 billion globally.

Healthcare and Financial Services deal counts doubled year over year, and infrastructure deal value reached $126.3 billion, a three-year high[8].

In Q4 2025, U.S. private equity deal value reached $1.2 trillion, the second time the figure has crossed the trillion-dollar mark (the first was 2021).

The quarter produced 150 megadeals worth $567.8 billion, U.S. dry powder reached a record $1.1 trillion, and exit counts grew at double-digit rates year over year for the first time in four years.

Construction and engineering broke out as a category (453 deals at $31.4 billion, with ConstructionTech at $4.1 billion against $1.2 billion the prior year).

Physician practice management roll-ups fell 50%.

In Europe, Apollo's €5.7 billion take-private of Athene's Pension Insurance Corporation was the quarter's largest take-private.

Asia rebalanced, with 75% of buyouts concentrated in consumer, technology, and industrial sectors[8].

In Q1 2026, the momentum was strong, as evident in the 5,100 transactions worth $481.6 billion, $2 trillion in global dry powder, and 22 megadeals at or above $10 billion - a record quarter, but the structural risks deepened.

Fundraising of $86 billion was flat year over year, with 2025 recorded as the weakest fundraising year since 2018. About 11,000 portfolio companies were held longer than five years, a hold-period overhang the secondary market is now absorbing.

The rescue act was visible in the secondary market where transactions reached $240 billion in 2025 (+48% year over year, a record), with forecasts of $300 billion annually and $327 billion in dedicated dry powder.

With high secondaries transaction foreasted for the next two years, Private credit assets under management crossed $2 trillion, with Moody's projecting $4 trillion by 2030 and $644 billion now in evergreen vehicles, a fund that accept new capital and process investor redemptions on a continuous basis, instead of operating on the closed-end ten-year cycle.

Not every private credit is smooth sailing. When the pressure on stock market increased - with the Iran war, Business development companies reported redemption requests at Blue Owl OTIC (40.7%), Blue Owl OCIC (21.9%), Cliffwater (14%), Apollo (11.2%), and BCRED (7.9%), with Saba Capital tendering at 65 to 80 cents on the dollar.

Q1 2026 opportunistic credit fundraising surpassed direct lending fundraising for the first time. Direct lending, the lower-risk segment that makes senior secured loans to private-equity-owned middle-market companies, had grown roughly four times over since 2018 on pension and insurance capital.

Opportunistic credit, the higher-return segment that includes mezzanine, rescue financing, special-situations debt, and commercial real estate credit in dislocated markets, raised more new capital in the quarter than direct lending did, anchored by Goldman Sachs at $13 billion in a new mezzanine fund and Benefit Street at $10 billion in a new commercial real estate credit fund [8]. The inversion reflects allocator preference shifting toward the higher-yield, more complex strategies in a cycle where mid-teens net returns are now harder to source from public markets.

The high-risk, high leverage arose from the optimistic projections in software valuations during 2022. Now, the software valuations are at 3.3 times against a five-year average of 7.1 times. PE firms are sitting on overvalued software portfolio companies with no IPO on sight. Only Alphabet's $32 billion acquisition of Wiz could set the largest venture-backed exit on record[8].

Implications for Booth and Stern candidates

The implication for Booth and Stern candidates is that the 2025 placement numbers (Booth at 5.3% into PE, Stern at 1.3%[1][2]) look paradoxical against a record PE deal environment, and the reason is the hiring channel.

KKR, Apollo, Blackstone, and Carlyle routed PE associate hiring through pre-MBA two-year analyst pipelines during this cycle, and held off on rebuilding post-MBA recruiting volume.

A PE-target candidate at either school should plan for a lateral path through PE-adjacent roles (Diversified Financial Services at Booth, Investment Banking at Stern), and target PE associate hiring in years two and three after graduation, when the 11,000 portfolio companies held longer than five years come up for exit and the megafunds reopen post-MBA classes to clear deal backlog.

Booth's 9.0% Diversified Financial Services placement positions the school well for this path. Stern's 28.0% IB placement does the same.

Venture Capital: AI Concentration at 81 Percent

In Q3 2025, global venture funding reached about $97 billion, a 38% increase year over year, with AI capturing roughly 46% of total global dollars and 57% of dollars committed in North America. The three largest rounds went to Anthropic at $13 billion, xAI at $5.3 billion, and Mistral AI at $2 billion, and eighteen companies together took close to a third of all global venture funding. Beneath the AI record numbers, circular investment patterns surfaced in which chip manufacturers and large corporate investors put capital into AI startups on the implicit expectation that the same dollars would return as chip and compute purchases [9].

In Q4 2025, the AI concentration extended into territory the venture capital industry had not previously seen. Global venture funding for the full year 2025 reached $425 billion, a 30% increase year over year, and AI alone captured $211 billion of that total. This was the first time a single theme had accounted for half of all venture dollars raised in a year. Anthropic's $15 billion round at a $183 billion valuation was the headline news for the quarter, while OpenAI's private-market valuation moved the valuation to $500 billion. The exit side reopened alongside it: venture-backed M&A reached $112.7 billion across about 1,000 deals, with Google's $32 billion acquisition of Wiz the largest venture-backed M&A on record [9].

In Q1 2026, the concentration of VC and PE funds reached its mathematical extreme. Global venture investment reached $297 billion in a single quarter, close to 70% of all 2025 venture spending into three months and the largest venture quarter on record, with AI capturing 81% of the total ($239 billion). The four largest rounds reached $188 billion between them, led by OpenAI at $122 billion and Anthropic at $30 billion.

Late-stage funding reached $244 billion, a 203% year-over-year increase, while seed dollars, mostly allocated to AI startups, rose 30% on a 31% drop in deal count - a split that confirmed that the funding ecosystem had narrowed at the top and thinned everywhere else. The top five venture firms took 73.1% of all limited-partner capital raised in the quarter, with Andreessen Horowitz's January 2026 fund alone accounting for more than 18% of all 2025 U.S. commitments. The distribution side gave the opposite reading - median distribution to paid-in capital for the 2017 vintage stood at 0.27x, that is the money returned to the money invested metric - the lowest since the 2008 financial crisis [9].

SpaceX filed its S-1 on May 20, 2026, and priced on June 11 at about $135 per share for a roughly $1.75 trillion valuation, the first live test of whether public markets would price an AI mega-round company at the level its last private round had set [9].

Implications for Booth and Stern candidates

The Class of 2025 VC placements (Booth 1.5%, Stern 1.7%[1][2]) are structurally explained by the fund concentration.

With five firms taking 73.1% of LP capital in Q1 2026 and the same firms preferring operator backgrounds (former founders, product leaders, and engineers) over the older MBA-to-VC associate path, the post-MBA VC associate seat that Sand Hill Road funded between 2018 and 2021 has largely closed.

The Booth and Stern candidates who did secure VC roles moved into corporate venture arms (Citi Ventures, Goldman Sachs growth equity, Morgan Stanley Counterpoint) and into family-office venture funds. These funds don't run formal on-campus recruiting calendars.

A VC-target candidate at either school should plan to spend the first three to five years post-MBA in an operator seat at a portfolio company, in product or strategy at a hyperscaler (Amazon, Microsoft, Alphabet, Meta), or in a corporate development role at an enterprise software company, and re-enter venture at the principal or partner level once the operator credential is in place.

The 2025 placement gap between Booth and Stern is not a verdict on the quality of either school's finance training. It is the snapshot of an industry in which megadeal flow concentrated in Investment Banking through AI boom.

Post-MBA hiring at the megafunds was paused on the PE side, and venture funding narrowed to five firms on the VC side.

The Q1 2026 trend lines suggest the IB calendar accelerates for the Class of 2026 at both schools, the PE calendar stays paused into the Class of 2027, and the VC calendar remains closed to the standard MBA-to-associate path through at least the SpaceX lockup expiry in December 2026[7][8][9].

Verdict for the Finance Applicant - Key Takeaways

- Choose NYU Stern if Investment Banking is your post-MBA target.

- Stern placed 28.0% of the Class of 2025 into Investment Banking, against Booth's 8.3%, at matching $175,000 medians and Stern's higher $57,448 average signing bonus[2], New York campus and IB Alumni should confirm that Stern is better suited for an Investment Banking career.

- Choose Chicago Booth if the post-MBA target is Diversified Financial Services, Investment Management, or a Consulting-finance hybrid. Booth placed 9.0% of the Class of 2025 into Diversified Financial Services at $215,000 total compensation, 5.3% into Investment Management at $205,000 total, and 36.7% into Consulting at $220,000 total[1].

- The optionality of Booth's curriculum, the STEM Analytic Finance concentration, and the school's quantitative orientation are the main reasons recruiters in these segments keep hiring at the Class of 2025 volumes.

- Booth should be your choice if you are an international student targeting U.S. finance roles. The Analytic Finance's STEM designation extends OPT from 12 to 36 months, which gives international finance candidates two additional H-1B lottery cycles.

- Stern's MBA carries a STEM designation through its Technology, Operations, and Statistics specialization. The route also exists at Stern, but the alignment with a finance concentration is weaker.

- Neither school is currently a high-probability Private Equity placement engine, in the sense of mid-market or megafund associate roles, since both schools placed below 6% into PE in 2025, and PE firms relied on pre-MBA pipelines during this cycle[1][2].

- A PE-focused candidate should prioritize Wharton or pre-MBA PE experience before considering the Booth versus Stern choice.

Methodology note

Numbers are reproduced verbatim from F1GMAT's 2025 and 2026 industry analyses, which in turn cite the schools' Class of 2025 Employment Reports.

Booth and Stern use slightly different reporting conventions.

Booth reports medians for both base and sign-on

Stern reports medians for base and averages for signing bonuses.

Stern class size is reported here in approximate terms because the school updates the figure during the academic year. F1GMAT's analysis confirms a finance-background share above 20% of the entering class[2][6]

References

- F1GMAT — Chicago Booth MBA Salary: By Industry (2025) (Analysis) ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- F1GMAT — NYU Stern MBA Salary: By Industry (2025) (Analysis) ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- Chicago Booth Full-Time MBA Employment Report (primary source) ↩ ↩

- NYU Stern MBA Employment Reports (primary source) ↩

- F1GMAT — MBA Salary, M7 and Top 20 MBA programs ↩

- Chicago Booth Class of 2027 Class Profile ↩ ↩ ↩

- F1GMAT Premium — Investment Banking Industry Trends (Q3 2025 to Q1 2026) ↩ ↩ ↩ ↩ ↩ ↩

- F1GMAT Premium — Private Equity Industry Trends (Q3 2025 to Q1 2026) ↩ ↩ ↩ ↩ ↩ ↩ ↩ ↩

- F1GMAT Premium — Venture Capital Industry Trends (Q3 2025 to Q1 2026) ↩ ↩ ↩ ↩ ↩ ↩

- Booth MBA Curriculum Analysis ↩ ↩ ↩

- Eugene F. Fama, Efficient Markets, and the Nobel Prize ↩

- Generalized Method of Moments Estimation ↩

- Myron S. Scholes ↩

- Richard H. Thaler ↩

- Aswath Damodaran ↩

- Edward I. Altman ↩

- Robert Whitelaw ↩

- Steven Kaplan ↩

that supports curiosity, inspires us to think more broadly, and take risks. At Booth, community is about collaborative thinking and learning from one another to better ourselves, our ideas, and the world around us.

that supports curiosity, inspires us to think more broadly, and take risks. At Booth, community is about collaborative thinking and learning from one another to better ourselves, our ideas, and the world around us.